How Much Investment Is Going into Building US Data Center Infrastructure?

14 Jul, 202611:06Key Takeaways: US data center infrastructure is projected to account for around $6.7 tr...

Key Takeaways:

- US data center infrastructure is projected to account for around $6.7 trillion in global compute power spend by 2030, including $5.2 trillion in AI infrastructure.

- Investment is flowing into buildings, power generation, transmission, cooling, networking, and the workforce to deliver projects.

- Hyperscalers, private equity, utilities, and energy investors are collectively shaping the industry across the full project stack.

- Specialist hiring has become a major part of delivery as projects are developed and expand across the United States.

US digital infrastructure has become one of the biggest infrastructure spend stories in the country, with capital streaming into data center construction, power systems, utilities, networking, and the specialist talent needed to make all of it work. The sheer amount of money involved is driven by AI and cloud demand, which require far more servers and floor space to keep growing, and by competitors wanting to maintain their top position in the ever-growing market.

The volume of investment in the US is also why the sceptics are getting harder to convince. If a sector is attracting capital on the scale of major industrial infrastructure, forcing utilities to rework long-range plans, and pulling in investors who would usually back energy, transport, or heavy industry, it becomes difficult to dismiss this shift as temporary.

Why the spend is so large

The largest driver of spend is AI, though cloud migration, enterprise demand, and digitization are still part of the picture. AI changes the economics of a data center because it needs denser compute, higher rack power, stronger cooling, bigger electrical systems, and more dependable energy access than traditional facilities. The cost isn’t just associated with the shell and IT fit-out, it’s the full infrastructure around it.

McKinsey estimates that worldwide compute power investment will reach around $6.7 trillion by 2030, with about $5.2 trillion linked directly to AI facilities. This is backed by a projected 156GW of AI-related data center infrastructure demand, explaining why the market is gaining interest. So, progression isn’t a normal tech cycle; it’s an industrial-scale race to build the physical backbone of AI. A growing number of operators now describe these facilities as “AI factories”, reflecting how the sector has moved from traditional enterprise data centers towards ones purposefully built for AI training and inference.

Data center investments and partnerships

One of the clearest changes in the market is how capital is structured. Data center investment and partnerships are being built around shared factors. Hyperscalers are working with multiple stakeholders because the size of these projects is too large for a single party to carry alone.

The US currently dominates the data center industry, representing over 40% of the global capacity according to S&P Global. And then with AI data centers expected to increase power demand by more than thirtyfold by 2035, it's understandable why investors view this as a key infrastructure sector.

The partnership model is changing how US data center projects are delivered:

- Hyperscalers are teaming up with hardware and infrastructure suppliers to secure compute capacity and cooling systems

- Private equity firms are backing greenfield campuses, acquisitions, and power-secure assets

- Utilities and energy developers are becoming strategic partners because speed to power is largely the main constraint

- Developers are signing long-term capacity contracts earlier, which changes the financing model before construction starts

And this impacts data center recruitment. A project built around partnerships needs talent across development, EPC, commissioning, energization, operations, and maintenance. It’s no longer enough to fill one role for one phase, companies need people who can support the entire program.

Another shift is the rise of modular and prefabricated construction. Investors and operators are increasingly relying on factory‑built power skids, cooling blocks, and standardized data halls to accelerate deployment and reduce supply chain risk. “Speed to market” has become a competitive differentiator, and modularization is now a core part of the delivery model.

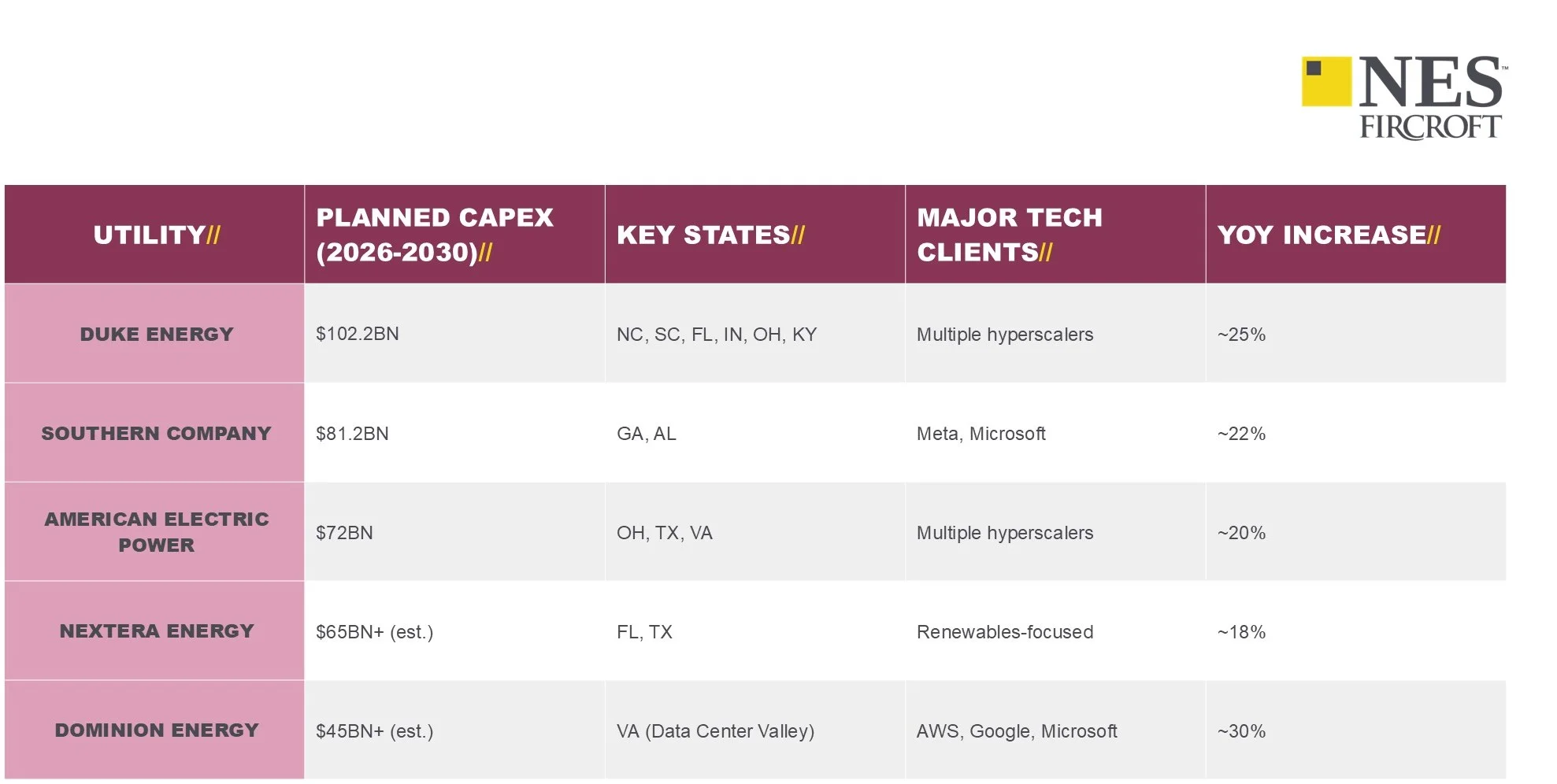

The clearest way to understand the investment mix is to look at where the money is going. The table below shows that spending isn’t concentrated in a single company or region; it spans multiple, which is exactly what you would expect in a sector with this level of long-term demand.

Source: Tech Insider

What is the role of ECP in data center development?

In this context, ECP refers to Energy Capital Partners, and its role sits right at the heart of the industry’s biggest bottleneck – power. Data centers need more than land and planning permission; they require constant, reliable electricity, transmission access, and, often, a route around utility queues.

ECP investors help build the power side through generation assets, renewables, storage, and behind-the-meter solutions that allow facilities to move forward with less dependence on congested grid capacity.

The broader point is that data center infrastructure development isn’t only a real estate or tech issue anymore; it’s an energy issue, too. Co-locating compute campuses with generation assets and securing long-term energy strategies are now common approaches to bypass grid delays and accelerate deployment.

What are the latest trends in data center infrastructure investments?

The strongest trend is that investment is more integrated, with capital moving beyond the building itself and into the full operating environment. IoT Analytics’ states that global data center infrastructure spend reached $290 billion in 2024 and is on course to pass $1 trillion annually by 2030. Alphabet, Microsoft, Amazon, and Meta invested nearly $200 billion in capex in 2024, and that figure is expected to rise further as AI buildouts continue.

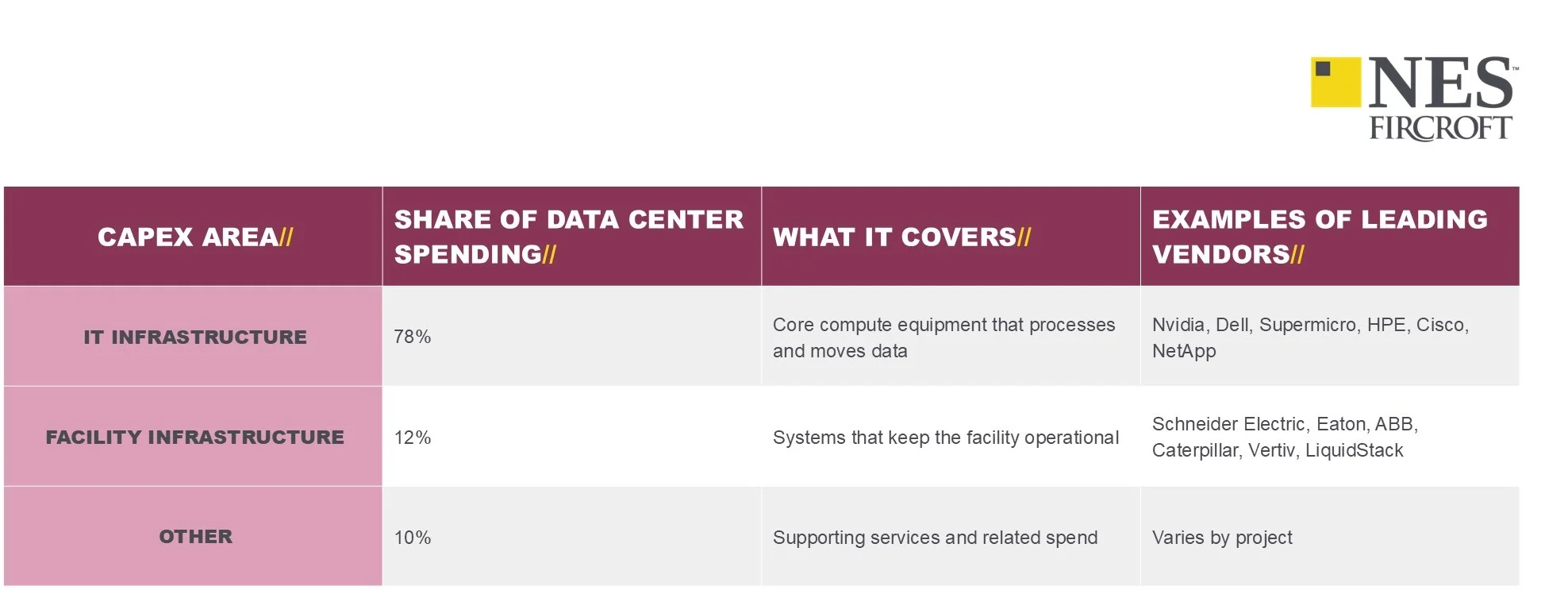

Here’s a table that shows where money tends to go inside the stack:

Source: IoT Analytics

The latest trends include:

- Power-first site selection is now normal, with access to electricity often mattering more than location alone

- Liquid cooling is moving into mainstream deployment because AI racks produce much higher heat loads than older enterprise systems

- Higher‑voltage architectures, new busbar systems, and more efficient power distribution models are being adopted to support extreme rack densities and reduce conversion losses

- Operators are being pushed to address sustainability, leading to greater interest in renewable PPAs, heat reuse, and low‑carbon backup systems

- Regional investment is spreading into key places such as Texas, Maryland, Virginia, Indiana, Ohio, and Kentucky, where land and energy access are more workable

- Private equity and infrastructure funds are treating data centers as durable assets

- Utility spending is climbing sharply, with US investor-owned utilities planning around 1.4 trillion in capex through 2030 to support AI demand

What is the overall economic impact of data centers in the tech industry?

Data centers in the US support GDP growth, local tax revenues, construction demand, supplier activity, and energy investment, while also increasing pressure on power systems, water use, and infrastructure planning.

Large facilities can create up to 1,500 construction jobs during buildout, while long-term operations usually require slightly smaller teams, made up of engineers, facility managers, technicians, and maintenance specialists. In Virginia, data center construction and operations contributed around $31 billion in supported economic output in 2023, which highlights how quickly these projects spread through local economies.

Employers now need a workforce that works across data center construction, power, transmission & distribution, renewables, commissioning, and technical operations, frequently on overlapping project schedules.

NES Fircroft: Leaders in Data Center Recruitment in the US

NES Fircroft has supported North America’s energy and infrastructure markets for more than 20 years, operating from over 15 offices across the US and Canada to provide local, insight-driven expertise. Our data center recruiters work closely with clients to supply the specialist talent needed across major projects. From project-based hiring to full workforce mobilization, we can ensure you meet aggressive build schedules and delivery milestones.

If you’re expanding AI‑ready campuses or building new facilities, our North American teams are ready to support your next phase of growth, contact us today.

FAQs

Is US digital infrastructure spend comparable to oil & gas?

Yes, in terms of scale and strategic importance, it increasingly is. Multi-trillion-dollar global investment, large utility capex commitments, and capital flowing into the entire project lifecycle resemble other major infrastructure sectors.

Why are data center investments and partnerships becoming common?

Because the projects are too large and too power-dependent to be delivered by singular companies, Hyperscalers, private equity firms, utilities, and infrastructure investors are joining forces to reduce risk and access to power.

What roles are hardest to hire in the data center market?

Electrical specialists, site engineers, project managers, commissioning professionals, and candidates with power or T&D experience are in especially strong demand. Roles that connect construction and energy tend to be the hardest to fill quickly.

How can NES Fircroft help with data center hiring?

NES Fircroft is a top data center recruitment agency in the US, providing scalable talent solutions across the project lifecycle, including contract specialists, permanent hires, and global mobility support. We also provide outsourced solutions such as Scope of Work, EOR and project RPO for large-scale hiring.